Strong results put fizz in Coca-Cola’s bottling plans

A Coca-Cola logo on a truck at a distribution center in Alexandria, Virginia October 16, 2012. Coca-Cola Co reported higher quarterly earnings on Tuesday, despite a hit from foreign exchange rates. The world's biggest soft-drink maker, with brands like Sprite, Fanta and Minute Maid, said net income was$2.31 billion, or 50 cents per share, in the third quarter that ended on Sept. 28, up from $2.22 billion, or 48 cents per share, a year earlier.

For South African investors with limited access to global consumer names on the local bourse, the prospect of a secondary listing by Coca-Cola HBC on the JSE seems meaningful. It would not just add another rand hedge but also import one of the world’s biggest Coca-Cola bottlers into local portfolios at precisely the moment the group is doubling down on Africa through its proposed acquisition of Coca-Cola Beverages Africa (CCBA).

To understand the appeal, it helps to remember how the Coca-Cola system actually works. The Coca-Cola Co owns the brands, concentrates and the overarching marketing strategy. The heavy lifting — turning concentrate into finished drinks, running high-speed bottling lines, packaging, warehousing, cold chain logistics and getting product onto store shelves — is handled by large franchise bottlers, which buy syrup concentrate from Coca-Cola, blend it with locally sourced water and sweeteners, carbonate it, bottle or can it, and then distribute the final product through vast retail networks.

These bottlers are capital-intensive, operationally complex businesses withformidable barriers to entry. Once embedded in a territory, with trucks,coolers and customer relationships in place, they resemble infrastructureassets as much as beverage companies. Done well, they throw off steady cashflows and high returns on capital.

HBC is widely regarded as one of the better operators in this global stable. Listed in London and Athens, it has built a reputation for tight cost control, sophisticated revenue growth management and disciplined capital allocation. Historically, its footprint spanned Central and Eastern Europe, Greece and parts of Western Europe, but over the past decade management has deliberately tilted the portfolio towards faster-growing emerging markets. Nigeria and Egypt are now important pillars of the story, and Africa is no longer a side bet but a core growth engine.

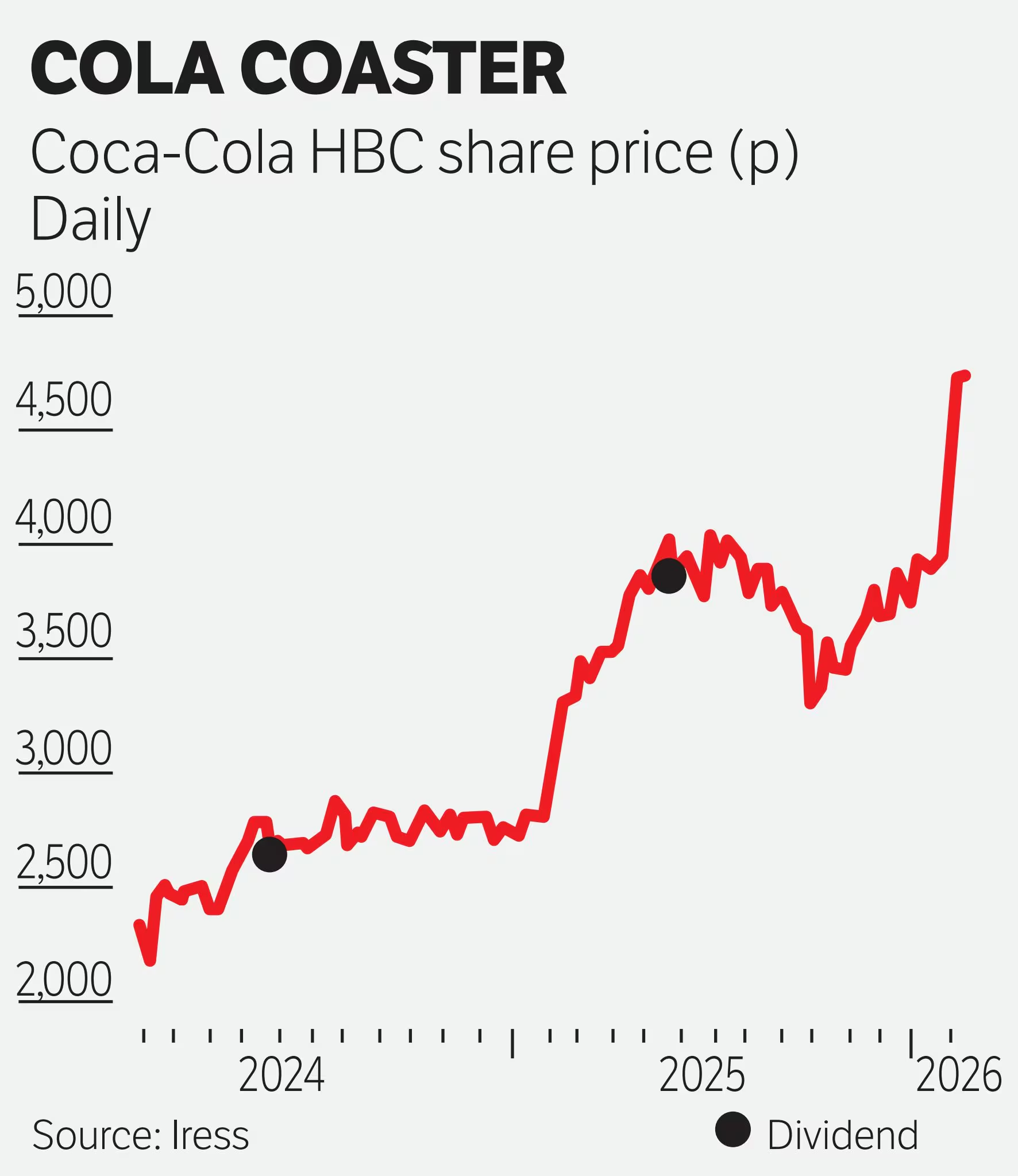

The newly released 2025 results reinforce why the business is so highly regarded. Group volumes rose 2.8% to just under 3-billion unit cases, while reported revenue climbed 7.9% to €11.6bn, with organic growth of 8.1%.Comparable increased 13.8% to €1.36bn and margins edged higher to 11.7%. Earnings per share grew nearly 20%, free cash flow remained robust at €700m and the balance sheet ended the year conservatively geared, with net debt to below one times.

The real standout, though, is the emerging markets segment, which houses most of HBC’s African exposure. There, organic revenue surged 13.2%,volumes grew 4.4% and comparable it jumped 23.2%, with margins expanding sharply. Nigeria delivered mid-single-digit growth in sparkling drinks such as Coca-Cola, Fanta and Sprite, alongside strong double-digit momentum in energy brands like Monster and Predator, while Egypt posted double-digit volume increases across categories. In other words, Africa is already the fastest-growing and most profitable part of the portfolio.

Overlay HBC’s systems — data analytics, pricing science, segmented execution — onto CCBA’s footprint and the potential for margin uplift is clear.

That context makes the proposed CCBA deal strategically obvious. Announced in October, HBC has agreed to acquire a 75% stake in CCBA for about $2.6bn, buying out existing shareholders The Coca-Cola Co and Gutsche Family Investments, with a path to full ownership eventually.

CCBA is the continent’s largest bottler, operating across more than a dozen markets — including South Africa, Kenya and Ethiopia — and accounting for more than 40% of all Coca-Cola products sold in Africa by volume. The combination, targeted for completion by the end of 2026, would create the world’s second-largest Coca-Cola bottling partner by volume and, more importantly, establish a single, fully integrated African platform.

At the recent results presentation, Coca-Cola HBC CEO Zoran Bogdanovic said the group is excited about the CCBA acquisition. “It’s a good business with strong brands, and we have great confidence in the opportunity to drive sustainable profit growth.”

From an investor’s perspective, the logic is compelling. Bottling is a scale game: procurement, manufacturing efficiency, route density and cooler placement all improve with size. Overlay HBC’s systems — data analytics, pricing science, segmented execution — onto CCBA’s footprint and the potential for margin uplift is clear. Management has already demonstrated in Nigeria and Egypt that it can win share and expand profitability in tough, inflationary markets. Replicating that formula across the broader African foot print could unlock substantial additional value.

This is also where the mooted JSE listing makes sense. If Africa becomes a much larger share of group earnings, a local shareholder base is strategically useful. It deepens relationships with regulators, governments and customers and provides South African institutions with a rare way to own a hard-currency, globally diversified consumer franchise without breaching exchange control limits.

Of course, bottling is not risk-free. It is exposed to currencies, input costs and sometimes messy politics. Nigeria and Egypt have both delivered their share of volatility. Yet HBC’s recent performance suggests it knows how to navigate these environments. Pricing discipline, package mix, energy drinks and premium categories have all helped protect margins, even as it invests heavily in capacity and marketing.

In the end, the investment case rests on a simple proposition. HBC has the hall marks of a long-term compounder: strong brands, entrenched distribution, high returns on capital and management that allocates cash sensibly. Bogdanovic disclosed guidance for 2026 that set organic revenue growth in the group’s 6%-7% medium-term target range as well as organic growth in the 7%-10% range.

The CCBA acquisition accelerates its exposure to one of the last underpenetrated beverage markets in the world. A secondary JSE listing would simply open the door for South Africans to ride along. For portfolios seeking global growth with an African twist, that combination may be hard to ignore.